Modest outlook for UK wood floorcoverings market as confidence and spending levels remain subdued

Published: 25 October 2019 - Neil Mead

The wood floorcoverings market is now more diverse than ever, with a high level of competition between the main product groups, as well as competing with floorcoverings products, such as floor tiles and LVT, according the latest research. In terms of supply, the market remains highly fragmented, with pricing being an important factor, as consumers increasingly seek value for money products and this has further intensified existing high levels of competition.

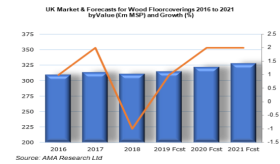

The wood floorings sector grew steadily from 2011 until 2017 but suffered marginal decline in 2018 and still remains well below the peak level of £385m achieved in 2007. Market trends had been positive since 2014, with growth strengthening until 2017, buoyed by rising consumer confidence as the economy improved and by growth in the housebuilding and wider construction sectors. However, the slowing of consumer and business confidence levels and a lower of investment and reduction in spending on non-essentials by consumers resulted in reversal of growth in 2018. Competition with other floorcoverings materials, especially LVT, has impacted the market with wood now marginally the third largest sector of the overall floorcoverings mix behind carpet and vinyl. In addition, the erosion of DIY skills within target market sectors has affected demand levels, particularly at the lower value end of the laminates sector.

Laminates currently account for the largest share of the wood floorcoverings sector, with around 59% of the market in value terms. Although the share held by laminates has declined over the last decade or so, it has remained relatively steady in recent years, with evidence that the product mix may now have stabilised. All product groups have increased sales in recent years supported by stronger brand recognition for some of the leading suppliers and the development of products with enhanced features, such as anti-slip and waterproofing, providing increased competition in the medium-upper market sectors.

The limited production facilities for laminates in the UK as well as the range of non-native species used in wood floors means that the UK has a significant trading deficit for wood floorcoverings. Imports of wood floorcoverings were on an upward trend until 2014, as the economy improved after the recession, with demand for floorcoverings boosted particularly by a recovery in both domestic and non-domestic construction activity and output. Since then, there has been a decline in imports, with particularly large falls in the 2017-18 period, reflecting ongoing factors, such as the volatility of global timber prices.

“The wood floorcoverings sector is forecast to show annual gains of around 2% in the period to 2023, however forecasting remains difficult in the current political and economic environment” said Jane Tarver of AMA Research. “The eventual conclusion of the Brexit process will be the key influence on the market with Sterling exchange rates likely to have more impact into the medium-term than has previously been the case”.

Any changes to import costs are likely to have a greater impact on margins and many suppliers may be forced to pass on increased costs. However, value growth is also likely to be stimulated by increase demand for FSC and PEFC certified timbers as environmental considerations become more prominent in the specification process.

Demand from both domestic and contract sectors is likely to be derived from higher value products as the market continues to distance itself from the “high volume, low value” perception previously associated with the laminates sector in particular. However, levels of consumer and business confidence into the short-medium term will be remain the key growth determinant.

The ‘Wood and Laminate Floorcoverings Market Report – UK 2019-2023’ is published by AMA Research, a leading provider of market research and consultancy services with 30 years’ experience within the construction and home improvement markets. The report is available now and can be ordered online at www.amaresearch.co.uk or by calling 01242 235724.